B2B payments are fundamentally different from consumer transactions. The amounts are larger, the approval requirements are more complex, the compliance burden is heavier, and the consequences of a failed or delayed payment carry real business risk.

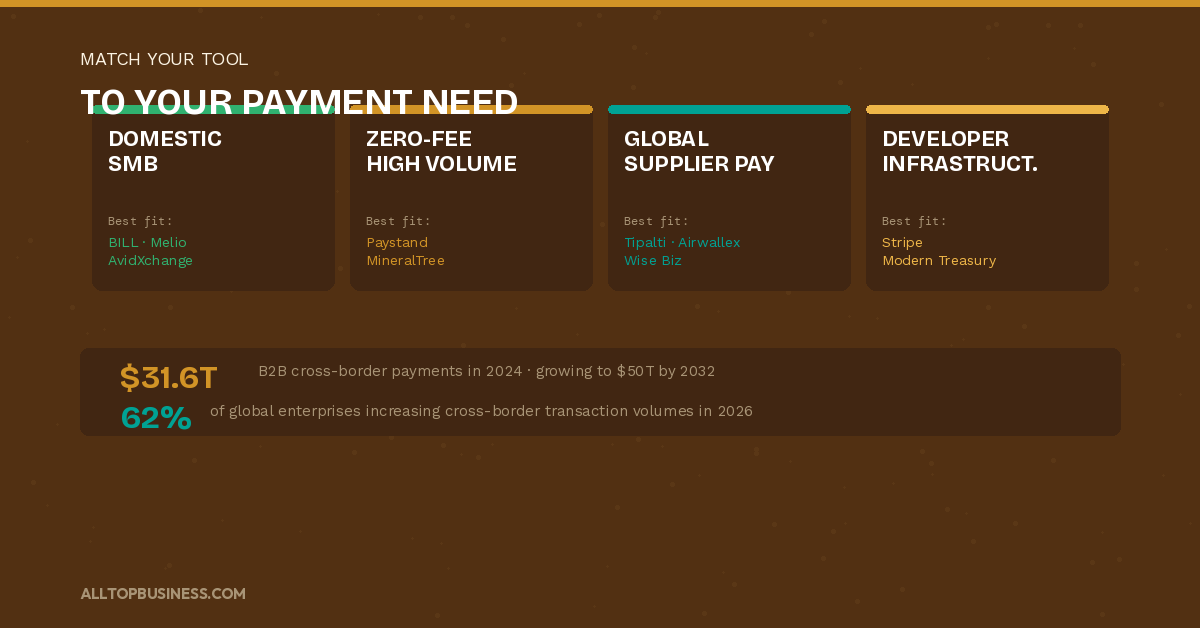

The B2B cross-border payments market alone reached $31.6 trillion in 2024 and is set to reach $50 trillion in 2032. Nearly 62% of global enterprises are increasing cross-border transaction volumes, while around 58% prioritize faster settlement and improved transparency. Yet most companies still process a significant share of their B2B payments through manual bank portals, email-based approval threads, and spreadsheet reconciliation.

The gap between best-in-class and average B2B payment operations is measurable. Around 49% of organizations report reconciliation inefficiencies, and 44% cite security concerns as primary payment challenges. Modern B2B payment software eliminates both by automating approval workflows, connecting directly to ERPs, and providing real-time payment status visibility that bank portals cannot match.

This guide covers the best B2B payment platforms evaluated against the same criteria. We assessed several B2B payment platforms to arrive at this list. Every entry includes real 2026 pricing, honest limitations, and a specific recommendation for who each tool fits.

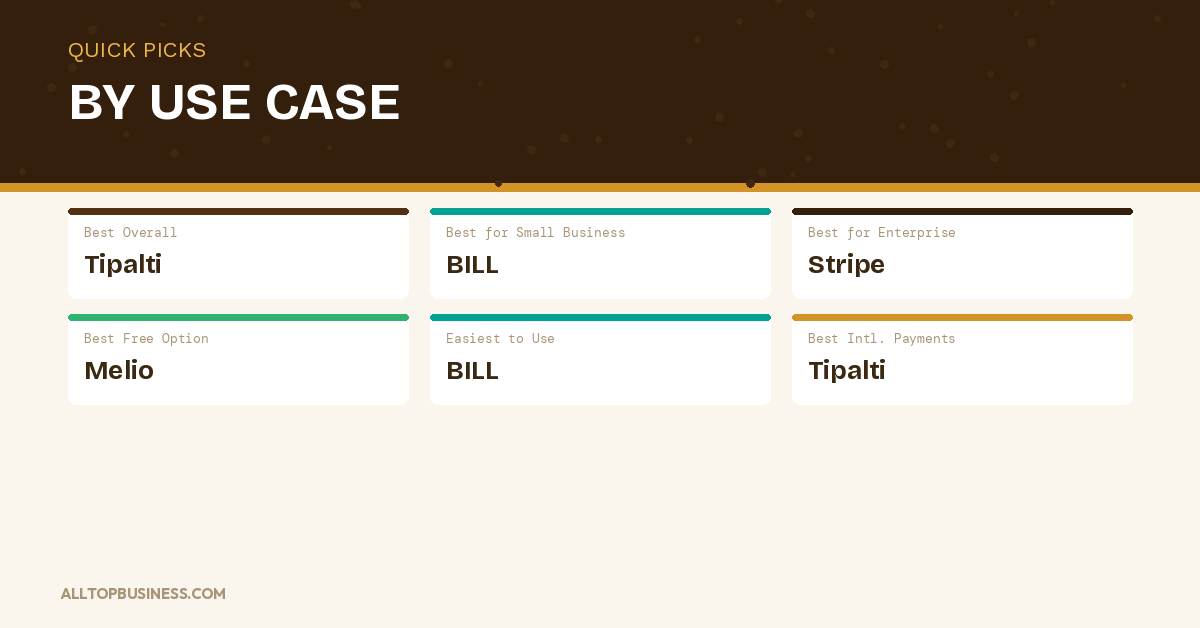

Best B2B Payment Software: Quick Picks

| Label | Pick |

|---|---|

| Best Overall | Tipalti — the most complete global B2B payments platform covering supplier onboarding, tax compliance, and mass payments across 196 countries |

| Best for Small Business | Melio — free core B2B payments with ACH and check options, no monthly subscription fee |

| Best for Enterprise | Stripe Treasury — programmable money movement infrastructure for enterprises building custom payment workflows |

| Best Free or Low-Cost Option | Melio — free ACH transfers with no monthly fee, pay-per-card-transaction model |

| Best for Ease of Use | BILL — the most beginner-friendly B2B payment platform for SMBs integrating with QuickBooks and Xero |

| Best for International Supplier Payments | Tipalti — 196-country payment coverage across 120 currencies with built-in tax and compliance automation |

How We Selected The Best B2B Payment Software Tools

Every platform was evaluated against six criteria:

- Payment rail coverage — ACH, wire transfer, virtual cards, checks, and international payment methods

- Automation depth — approval workflows, payment scheduling, fraud controls, and reconciliation automation

- Global capability — multi-currency support, cross-border payment coverage, and local compliance

- ERP and accounting integration — bidirectional sync with major ERP and accounting platforms

- Security and fraud controls — OFAC screening, dual controls, payment validation, and audit trails

- Pricing transparency — actual cost data from public sources and verified industry benchmarks

Best B2B Payment Software: Comparison Table

| Tool | Best For | Starting Price | Free Plan | Key Integration |

|---|---|---|---|---|

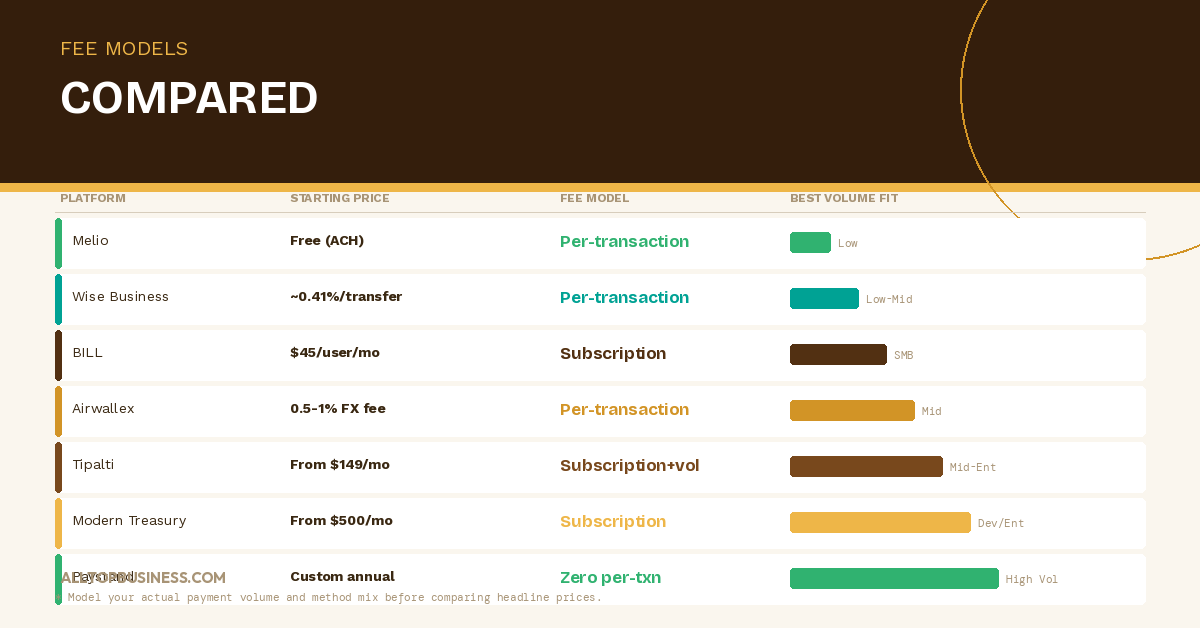

| Tipalti | Global supplier payments and mass payables | From $149/mo | No | NetSuite, SAP, QuickBooks, Oracle |

| BILL | SMB AP and AR payment automation | From $45/user/mo | No | QuickBooks, Xero, NetSuite |

| Melio | Very small businesses that need free ACH payments | Free core | Yes | QuickBooks, Xero |

| Stripe | Developer-first payment infrastructure | Pay-per-transaction | No | Most ERPs via API |

| Airwallex | Global B2B payments with multi-currency accounts | Free to open | No | Xero, QuickBooks, NetSuite |

| Wise Business | International supplier payments at low FX rates | Free to open / fees per transfer | No | QuickBooks, Xero |

| Paystand | Zero-fee bank-to-bank B2B payments | Custom | No | NetSuite, Salesforce, SAP |

| AvidXchange | Mid-market AP automation and B2B payments | Custom | No | NetSuite, Sage Intacct, QuickBooks |

| Modern Treasury | Developers building custom payment operations | From $500/mo | No | Most banks via API |

| Bottomline Technologies | Enterprise B2B payments and cash management | Custom | No | SAP, Oracle, Microsoft |

| MineralTree | Mid-market AP payments with virtual card rebates | Custom | No | NetSuite, Sage Intacct, QuickBooks |

| Convera | Enterprise cross-border B2B payments | Custom | No | SAP, Oracle, ERP agnostic |

| Ebury | SME international payments and trade finance | Custom | No | Xero, QuickBooks, Sage |

1. Tipalti

The most complete global B2B payables automation platform

Tipalti covers the entire supplier payment lifecycle — from self-service supplier onboarding through W-9 and W-8 tax form collection, invoice processing, payment execution across 196 countries in 120 currencies, and ERP reconciliation — in a single platform. No other tool on this list matches this end-to-end coverage for global payables.

The platform’s compliance automation is its primary differentiator. OFAC and sanctions screening run on every payment before execution. Tax form collection from suppliers is automated through a self-service portal, eliminating the manual back-and-forth that delays onboarding. Payment risk scoring flags anomalies before funds leave the account. For mid-market and enterprise companies paying large numbers of international suppliers, Tipalti removes compliance risks that manual payment processes create without adequate controls.

Tipalti pricing starts at $149 per month base and scales with payment volume. Enterprise implementations with full ERP integration typically cost $25,000 to $75,000 annually. Implementation runs 6 to 12 weeks for full deployment.

What it does well:

- End-to-end supplier payment lifecycle from onboarding through reconciliation

- Automated tax form collection — W-9 and W-8 handled through supplier self-service portal

- OFAC and sanctions screening on every outgoing payment

- Payment execution across 196 countries in 120 currencies via ACH, wire, PayPal, and local rails

- Native ERP integration with NetSuite, SAP, QuickBooks, and Oracle

Where it falls short:

- Implementation of 6 to 12 weeks and meaningful professional services costs

- Pricing scales with payment volume — high-volume teams should model total cost carefully

- Less suitable for companies with primarily domestic payment needs

Pricing: Base from $149/month. Total annual cost scales with payment volume and ERP integration complexity.

Best for: Mid-market and enterprise companies with $50M+ in revenue that pay large numbers of international suppliers and need end-to-end payables automation with built-in tax compliance and sanctions screening.

2. BILL

The most accessible B2B payment platform for small businesses

BILL is the most widely adopted B2B payment automation tool for small businesses, combining accounts payable, accounts receivable, and basic payment processing in a single platform. Its 7 million+ member network means many suppliers are already registered, which speeds payment delivery and eliminates manual banking detail collection.

The platform supports ACH, check, and international wire payments. The vendor payment workflow covers invoice capture, approval routing, and payment execution with sync back to QuickBooks or Xero. For small finance teams that need to move off manual bank portals without a complex implementation project, BILL provides the fastest path to automated B2B payments.

BILL starts at $45 per user per month for the Essentials plan, with higher tiers adding more advanced workflow features.

What it does well:

- 7 million+ member network for faster supplier payment delivery

- Covers both AP and AR payment workflows in one platform

- Strong QuickBooks and Xero integration with automatic sync

- Invoice capture and approval routing alongside payment execution

- Fast implementation — most SMBs operational within one to two days

Where it falls short:

- International payment capabilities are more limited than Tipalti or Airwallex

- Less depth in complex multi-entity or high-volume payment operations

- Per-user pricing adds up for larger teams

Pricing: From $45/user/month. Essentials, Team, and Corporate tiers with increasing functionality.

Best for: Small businesses with 5 to 100 employees that want the simplest path from manual bank portal payments to automated AP and AR payment workflows with direct accounting software integration.

3. Melio

The best free B2B payment tool for very small businesses

Melio is a zero-fee-to-start B2B payment platform that allows small businesses to pay vendor invoices via ACH bank transfer at no cost or via credit card with a 2.9% fee passed to the payer. There is no monthly subscription. The platform integrates with QuickBooks and Xero, syncing bills and payment records automatically.

For very small businesses that need to stop writing checks and wiring from bank portals but are not ready for a paid subscription platform, Melio solves the problem immediately at zero software cost. The trade-off is that Melio is a payments tool, not a payments automation platform. There is no invoice capture, no complex approval routing, and no multi-entity support.

What it does well:

- Zero monthly subscription fee — core B2B payments at no software cost

- Free ACH transfers with no per-transaction fee for bank payments

- Fast setup — operational in minutes for very small teams

- QuickBooks and Xero sync for automatic accounting records

- Schedule payments in advance for better cash flow management

Where it falls short:

- No invoice capture, complex approval workflows, or procurement integration

- Not suitable for companies with high payment volumes or complex requirements

- International payment options are limited

Pricing: Free core. 2.9% fee for credit card payments.

Best for: Freelancers, sole proprietors, and very small businesses that want to pay vendors digitally via ACH at zero software cost with basic QuickBooks or Xero integration.

4. Stripe

The best developer-first B2B payment infrastructure for companies building custom workflows

Stripe is the most widely used payment infrastructure platform globally, covering card processing, ACH, bank debits, and international payment methods through a developer-first API. For B2B use cases, Stripe supports invoice creation and payment, subscription billing, ACH debit pull payments, and programmatic payment orchestration through Stripe Treasury.

Stripe’s strength in B2B contexts is its flexibility. Any payment workflow a finance or product team can specify, Stripe can execute. For companies building custom order-to-cash workflows, embedded payment experiences in SaaS products, or marketplace payment distribution, Stripe provides the infrastructure layer without requiring off-the-shelf product constraints.

The honest limitation is that Stripe is infrastructure, not a complete B2B payment solution. Building a production-grade B2B payment workflow on Stripe requires developer resources and meaningful engineering investment.

What it does well:

- The most comprehensive payment API available — supports virtually any B2B payment workflow

- Global coverage across 46 countries with local payment method support

- Stripe Treasury for programmable money movement and embedded financial services

- Strong fraud detection through Stripe Radar with machine learning models

- Transparent per-transaction pricing without monthly minimums

Where it falls short:

- Requires developer resources to implement — not a self-service finance team tool

- No built-in AP automation, approval workflows, or supplier management

- Customer support is primarily documentation-driven rather than human-assisted

Pricing: 2.9% + $0.30 per successful card charge. ACH credit from 0.8% capped at $5. Custom pricing for high-volume businesses.

Best for: Technology companies, SaaS platforms, and enterprises with development resources that need programmable payment infrastructure rather than an off-the-shelf B2B payment product.

5. Airwallex

The best platform for international B2B payments with multi-currency accounts

Airwallex is a global financial platform that combines multi-currency business accounts, international payment execution, FX conversion, and corporate card management in a single platform. Opening an Airwallex account is free, and the platform supports holding balances in over 23 currencies without conversion fees for same-currency transfers.

For businesses making regular payments to international suppliers, Airwallex removes two layers of cost: bank FX markups on currency conversion and international wire transfer fees for outbound payments. The platform executes payments via local payment rails in 150+ countries rather than routing through expensive correspondent banking networks.

Airwallex integrates with Xero, QuickBooks, and NetSuite, syncing multi-currency payment data back to accounting software automatically.

What it does well:

- Multi-currency accounts in 23+ currencies with no account opening fee

- Local payment rail execution in 150+ countries eliminates correspondent banking fees

- Competitive FX rates significantly below standard bank rates

- Corporate cards issued in local currencies for international team spending

- Strong API for companies wanting to automate international payment workflows

Where it falls short:

- Less depth in AP automation, approval workflows, and supplier management versus Tipalti

- Customer support receives mixed reviews for complex issues

- Less suitable for companies with primarily domestic US payment needs

Pricing: Free to open. FX conversion fees from 0.5% to 1% above the mid-market rate. Payment fees vary by destination and method.

Best for: Mid-market companies with regular international supplier payments that want to reduce FX costs and wire transfer fees through local payment rails and multi-currency accounts.

6. Wise Business

The best low-cost international B2B payment platform for SMBs

Wise Business is the business-facing product of Wise, built on the same transparent FX rate infrastructure that has made Wise the most recognized brand in low-cost international money transfers. The platform supports sending payments to 160+ countries with fees typically 2 to 6 times lower than traditional bank wire transfers, using the mid-market exchange rate rather than the inflated rates most banks apply.

Wise Business accounts hold balances in 40+ currencies and generate account details in multiple countries, making it straightforward to receive payments from international customers or pay overseas suppliers in their local currency. The QuickBooks and Xero integration syncs payment records automatically.

What it does well:

- The most transparent international payment pricing — exact fees shown before every transfer

- Mid-market FX rates with no hidden currency conversion markup

- Multi-currency account details in major markets for receiving international payments

- Fast international transfers — many corridors settle within hours rather than days

- Strong QuickBooks and Xero integration for accounting sync

Where it falls short:

- No AP automation, approval workflows, or supplier management functionality

- Transaction limits apply in some corridors and for some account tiers

- Less suitable for very high-value B2B transactions where dedicated banking relationships add value

Pricing: Free to open. Transfer fees are approximately 0.41%, depending on the currency corridor.

Best for: SMBs and growing mid-market companies that make regular international supplier payments and want to reduce FX costs and wire transfer fees without enterprise payment infrastructure investment.

7. Paystand

The best B2B payment platform for companies that want to eliminate transaction fees

Paystand operates on a fundamentally different pricing model from most B2B payment platforms. Rather than charging per-transaction fees, Paystand charges a flat annual subscription and processes payments directly bank-to-bank — eliminating the per-transaction interchange and processing fees that compound into high costs for high-volume payment operations.

For companies processing significant B2B payment volumes where credit card and ACH transaction fees represent a meaningful cost line, Paystand’s zero-fee model can produce meaningful annual savings. The platform also supports virtual card issuance for supplier payments, which generates rebate income on a portion of the payment portfolio.

Paystand integrates natively with NetSuite, Salesforce, and SAP, and its payment network covers ACH, credit card, and bank-to-bank payment methods.

What it does well:

- Zero per-transaction fees after flat annual subscription — meaningful cost savings for high-volume payers

- Bank-to-bank payment network eliminates interchange fees on eligible transactions

- The virtual card program generates rebate income on a portion of the payment volume

- Strong NetSuite and Salesforce integration

- Real-time payment status tracking and automated reconciliation

Where it falls short:

- Zero-fee model requires suppliers to accept bank-to-bank payments — not all supplier bases will adopt this

- Custom annual pricing requires a sales conversation

- Less depth in international payment coverage compared to Tipalti or Airwallex

Pricing: Custom annual subscription. Zero per-transaction fees after subscription.

Best for: Mid-market and enterprise companies with high domestic B2B payment volumes that want to reduce or eliminate per-transaction fees by shifting to a subscription-based bank-to-bank payment model.

8. AvidXchange

The best AP automation and B2B payment platform for mid-market companies

AvidXchange is a purpose-built AP automation and B2B payment platform for mid-market companies. It covers invoice capture, approval routing, and payment execution in a single system designed specifically for companies with 50 to 1,000 employees that have outgrown manual AP but do not need enterprise-scale payment infrastructure.

The platform’s payment network covers ACH, virtual card, and check payments, with automatic payment method optimization that routes each payment through the most cost-effective channel. Virtual card payments generate rebate income for companies where supplier adoption allows card payments.

AvidXchange has strong integration with NetSuite, Sage Intacct, and QuickBooks, and its implementation timeline is typically 6 to 10 weeks for mid-market deployments.

What it does well:

- Purpose-built for mid-market AP automation and payment processing

- Automatic payment method optimization across ACH, virtual card, and check

- Virtual card rebate program for eligible supplier payments

- Strong NetSuite, Sage Intacct, and QuickBooks integration

- Good implementation support with dedicated onboarding resources

Where it falls short:

- Less suitable for companies with significant international payment requirements

- Custom pricing requires a sales conversation

- Less suitable for very large enterprise organizations with global payment complexity

Pricing: Custom pricing based on invoice volume and payment methods.

Best for: Mid-market companies with 50 to 500 employees that want AP automation and domestic B2B payment execution with virtual card rebates in a single mid-market-priced platform.

9. Modern Treasury

The best payment operations platform for developers and fintech-adjacent businesses

Modern Treasury is a payment operations platform that abstracts the complexity of connecting to multiple banks and payment rails behind a single, clean API. Where Stripe focuses on card-based payments, Modern Treasury focuses on bank payments — ACH, wires, RTP (real-time payments), and international transfers — with a developer-friendly interface and real-time payment status tracking.

For companies building internal payment automation systems, fintech products, or treasury management workflows that require programmatic control over bank payment execution, Modern Treasury provides a significantly cleaner developer experience than connecting directly to individual bank APIs.

Pricing starts at $500 per month for the Starter plan, which targets companies processing moderate payment volumes with developer-driven implementations.

What it does well:

- Single API connecting to multiple banks and payment rails simultaneously

- Real-time payment status and ledger tracking across all payment types

- Strong support for RTP (real-time payments) and FedNow payment rails

- Clean developer documentation with strong implementation support

- Good reconciliation automation for complex multi-account payment operations

Where it falls short:

- Requires developer resources — not a self-service finance team platform

- $500/month minimum pricing is higher than some developer-focused alternatives

- Less suitable for companies that need pre-built AP automation and supplier management

Pricing: Starter from $500/month. Scale and Enterprise custom pricing.

Best for: Fintech companies, treasury technology teams, and developer-driven businesses that need programmable access to bank payment rails with real-time ledger tracking and strong API documentation.

10. Bottomline Technologies

The best B2B payment and cash management platform for enterprise financial institutions

Bottomline Technologies is an enterprise financial technology platform covering B2B payments, cash management, payment fraud prevention, and financial messaging. It is particularly strong for financial institutions, banks, and large corporate treasuries that need payment infrastructure at enterprise scale with strong regulatory compliance coverage.

The platform supports SWIFT, ACH, wire, and international payment execution with advanced fraud prevention through its SWIFT intelligence and payment fraud monitoring tools. For enterprise organizations managing high-value payment flows where a single fraudulent transaction can represent significant financial exposure, Bottomline’s fraud prevention capabilities justify the enterprise investment.

What it does well:

- Enterprise-grade payment fraud prevention with SWIFT intelligence monitoring

- Comprehensive payment rail coverage, including SWIFT, ACH, wire, and international

- Strong regulatory compliance for financial institutions and large corporates

- Cash management and treasury integration alongside payment execution

- Proven at enterprise and financial institution scale globally

Where it falls short:

- Not suitable for SMBs or companies without enterprise payment volumes

- Custom enterprise pricing at the higher end of the market

- Implementation complexity requires dedicated project resources

Pricing: Custom enterprise pricing.

Best for: Enterprise corporations, financial institutions, and large corporate treasuries managing high-value B2B payment flows where fraud prevention and regulatory compliance at scale are primary requirements.

11. MineralTree

The best mid-market B2B payment platform focused on payment execution and virtual card rebates

MineralTree focuses specifically on the payment execution side of B2B payables — automating the payment run and optimizing payment method mix to maximize virtual card rebate income. For mid-market companies that already have invoice processing under control but still run payment batches manually through their bank portal, MineralTree removes that last manual step.

The virtual card program automatically issues single-use virtual cards for eligible supplier payments, generating rebate income that, for many companies, offsets a meaningful portion of the platform cost. Payment fraud controls include dual approval requirements and payment limit rules that prevent unauthorized payments.

What it does well:

- Virtual card rebate program generates income on eligible supplier payments

- Payment method optimization across ACH, virtual card, and check is automatic

- Strong NetSuite, Sage Intacct, and QuickBooks integration

- Payment fraud controls with dual approval and payment limit enforcement

- Faster implementation than full AP automation platforms

Where it falls short:

- Less depth in invoice capture and coding versus Stampli or DOKKA

- Less suitable for companies with high international payment requirements

- Custom pricing requires a sales conversation

Pricing: Custom pricing based on payment volume.

Best for: Mid-market companies with established invoice processing workflows that want to automate the payment execution step and generate virtual card rebate income on a portion of their supplier payment portfolio.

12. Convera

The best enterprise cross-border B2B payment platform for global trade operations

Convera is a specialist cross-border payment provider that handles high-value international B2B transactions for enterprise organizations engaged in global trade. Formerly Western Union Business Solutions, Convera processes over $100 billion in annual payment volume across more than 200 countries and territories.

The cross-border payments market reached $238 billion in 2026 and is expected to grow at a 7.16% CAGR, reaching $336 billion by 2031. Within that market, Convera serves the enterprise segment with dedicated FX risk management services, forward contracts for locking in exchange rates on future supplier payments, and a payments infrastructure that handles the compliance complexity of cross-border trade at scale.

For more on managing FX exposure on international supplier payments, read our guide on FX risk management for companies paying overseas suppliers.

What it does well:

- $100B+ annual payment volume across 200+ countries — proven cross-border scale

- FX risk management services, including forward contracts and rate hedging

- Dedicated relationship managers for enterprise payment programs

- Strong compliance and regulatory coverage for cross-border trade

- ERP-agnostic integration approach supporting most major systems

Where it falls short:

- Less suitable for companies with primarily domestic payment needs

- Custom pricing requires an enterprise sales conversation

- Less technology-forward than newer fintech platforms for developer-driven use cases

Pricing: Custom pricing based on payment volume and currency corridors.

Best for: Enterprise organizations engaged in significant cross-border trade that need a specialist payment partner with FX risk management capabilities and dedicated relationship support for high-value international transactions.

13. Ebury

The best B2B payment and trade finance platform for SMEs with international operations

Ebury combines international B2B payment execution with trade finance services — letters of credit, invoice financing, and supply chain finance — for small and mid-sized businesses engaged in international trade. For SMEs that need both FX hedging and trade financing alongside international payment execution, Ebury provides a single commercial relationship covering all three needs.

The platform offers forward contracts for locking in exchange rates on future international supplier payments, multi-currency accounts in over 29 currencies, and dedicated relationship managers for accounts above a certain payment volume threshold.

What it does well:

- Combines FX hedging, international payments, and trade finance in one relationship

- Forward contracts for managing currency risk on future supplier payments

- Multi-currency accounts in 29+ currencies

- Letters of credit and supply chain finance for trade-intensive SMEs

- Dedicated relationship managers at higher payment volume tiers

Where it falls short:

- Less technology-forward than Airwallex or Wise for self-service international payments

- Trade finance products add complexity that pure payment-only businesses do not need

- Less suitable for companies without international trade finance requirements

Pricing: Custom pricing based on payment volume and services used.

Best for: SMEs engaged in international trade that need FX hedging, letters of credit, and trade finance alongside international payment execution from a single specialist provider.

How to Choose the Best B2B Payment Software

The B2B payment market is fragmented because different payment problems require genuinely different solutions. Four questions cut through the complexity.

Domestic-only or international payments?

For primarily domestic US payments, BILL, Melio, AvidXchange, MineralTree, and Paystand cover the core use cases efficiently. For regular international supplier payments, Tipalti, Airwallex, Wise Business, Convera, or Ebury address the cross-border complexity that domestic-first platforms handle poorly.

Do not pay for global infrastructure you do not need, but do not underestimate international payment complexity if you have it.

Volume and automation requirements

Very small businesses processing under 50 payments per month are well-served by Melio or BILL at low or zero cost. Mid-market companies processing 100 to 2,000 payments per month get the best value from Tipalti, AvidXchange, or MineralTree.

Enterprise organizations with complex payment orchestration requirements should evaluate Bottomline, Convera, or build on Stripe or Modern Treasury with internal development resources.

Fee model preference

Per-transaction fee models (Stripe, Melio for card, Airwallex, Wise) work well when payment volumes are moderate. Subscription-based models (Paystand, Modern Treasury) produce better economics at high volumes.

Tipalti and BILL charge subscription plus volume-based fees. Map your actual payment volume and method mix against each pricing model before comparing headline numbers.

Security and compliance requirements

OFAC screening, dual payment controls, and payment fraud prevention should be non-negotiable for any company above SMB scale. Tipalti, Bottomline, and AvidXchange all include these controls natively.

BILL and Melio provide basic controls appropriate for SMB use. Stripe and Modern Treasury require configuration of fraud rules by the implementing development team.

Frequently Asked Questions

What is the best B2B payment software overall?

Tipalti is the strongest all-around choice for mid-market and enterprise companies with international supplier payment requirements. For SMBs, BILL is the most complete starting point.

For very small businesses needing free ACH payments, Melio removes the cost barrier entirely. For companies primarily focused on reducing international payment costs, Airwallex or Wise Business delivers the best FX rates and lowest transfer fees.

What is the difference between B2B payment software and a payment gateway?

A payment gateway processes card transactions between a buyer and a merchant at the point of sale. B2B payment software manages the entire supplier payment lifecycle — invoice capture, approval routing, payment execution via multiple rails including ACH and wire, and reconciliation back to the ERP.

B2B payments are higher-value, more complex, and require workflow controls that consumer payment gateways are not designed to provide.

How much does B2B payment software cost?

Melio is free for ACH payments with no monthly subscription. BILL starts at $45 per user per month. Tipalti starts at a $149 per month base with volume-based scaling. AvidXchange and MineralTree are custom-priced in the mid-market range.

Enterprise platforms like Bottomline and Convera require custom enterprise pricing. Always model total cost including transaction fees, not just the monthly subscription price.

What payment rails do B2B payment platforms support?

Most platforms support ACH (US domestic bank transfers), wire transfers, and virtual card payments. International platforms like Tipalti, Airwallex, and Convera add local payment rails in each destination country, which are typically faster and cheaper than international wire transfers routed through correspondent banks.

Real-time payment rails, including RTP and FedNow, are supported by Modern Treasury and increasingly by other platforms as US adoption grows.

How do virtual card rebates work in B2B payments?

Virtual cards are single-use card numbers generated for specific supplier payments. When a supplier accepts payment by virtual card, the paying company earns interchange rebate income — typically 1% to 2% of the payment value — from the card network.

Platforms like MineralTree, AvidXchange, and Tipalti automatically identify suppliers willing to accept virtual card payments and route those transactions through card rails to generate rebate income. For companies with large supplier bases, this can offset a significant portion of platform costs.

Final Verdict

Tipalti is the strongest choice for mid-market and enterprise companies making regular international supplier payments — its end-to-end coverage of supplier onboarding, tax compliance, and global payment execution is unmatched at this price point. BILL is the right starting point for SMBs that want AP and AR payment automation with direct QuickBooks or Xero integration.

For international payment cost reduction without full AP automation, Airwallex and Wise Business both deliver FX rates significantly below bank rates. Paystand is the right choice when eliminating per-transaction fees is the primary objective. AvidXchange hits the mid-market sweet spot for domestic AP automation with virtual card rebates.

For developer-driven payment operations, Stripe and Modern Treasury provide the most flexible infrastructure. For enterprise cross-border trade with FX risk management requirements, Convera or Ebury brings specialist expertise that general payment platforms cannot match.

The most costly B2B payment mistake is paying per-transaction fees on high volumes when a subscription model would be significantly cheaper. Model your actual payment volume, method mix, and international requirements before committing to a platform.

For more B2B finance and software reviews, browse the AllTopBusiness blog. Have a specific B2B payment question for your team? Contact us directly.

I’m Adeyemi Adetilewa, a Content Marketing and SEO Specialist, Digital Strategist, Entrepreneur, and the Editor of AllTopBusiness.com. With over 13 years of experience helping businesses scale through content-driven growth, I’m happy to share all the top business tools I have discovered with you here.