FX risk management for supplier payments comes down to four steps: map your currency exposure, choose the right hedging tools (forward contracts, window forwards, or options), select a platform to execute and track hedges, and write a one-page FX policy that makes the process repeatable.

The best FX risk management tools for mid-market companies include Kyriba, GTreasury, Nomentia, Corpay, and Xe for Business. This guide covers all of it in plain terms.

You agree on a price with your overseas supplier in euros. You think the exchange rate looks acceptable today. Three months later, when the invoice lands, the euro has strengthened 6% against the dollar, and your gross margin on that order has effectively been cut in half before a single unit ships.

That is not a finance problem. That is a cost control problem. And it happens to thousands of U.S. companies every year because FX risk management gets treated as something only large multinationals need to worry about.

It does not. Any company that pays overseas suppliers in a foreign currency, buys materials priced in a non-dollar currency, or operates across multiple countries is exposed to foreign exchange risk. The only question is whether that exposure is being managed deliberately or absorbed silently into your margins.

This guide gives you a practical, plain-English framework for managing FX risk on supplier payments from mapping your exposure to choosing the right hedging tools to building a simple policy your team can follow without a full treasury department.

For a broader context on how FX risk fits within the overall treasury function, read our guide on what treasury management is and how it works.

What is FX Risk and Why Does It Matter for Supplier Payments?

Foreign exchange risk, also called currency risk, is the exposure a business has to losses or reduced margins caused by movements in exchange rates. For a company that pays overseas suppliers, three specific types of FX risk matter:

Transaction risk is the most immediate. It arises when you have a committed obligation to pay a supplier in a foreign currency at a future date, but you have not yet locked in the exchange rate. Between the time you place an order and the time you make the payment, the rate can move in either direction. A strengthening foreign currency means you pay more in dollars than you budgeted.

Economic risk is broader. It refers to the impact that long-term currency movements have on your business’s competitive position. If the currencies of your supplier countries strengthen significantly against the dollar over time, your cost of goods rises relative to competitors who source domestically or from lower-cost currency regions.

Translation risk applies primarily to companies with overseas subsidiaries. When foreign entity financials are converted back to USD for consolidated reporting, exchange rate movements affect the reported numbers even if no actual cash changed hands.

For most U.S. mid-market companies paying overseas suppliers, transaction risk is the primary concern. That is where this guide focuses.

Step 1: Map Your FX Exposure

You cannot manage what you cannot see. Before you decide on a hedging strategy or choose a tool, you need a clear picture of your actual currency exposure.

Start with a simple exposure map that captures the following for each major supplier currency:

| Exposure Type | Example | Data to Capture |

|---|---|---|

| Confirmed payables | EUR invoices from a European manufacturer | Currency, amount, due date, vendor |

| Open purchase orders | CNY POs for next quarter’s production run | Currency, amount, expected payment date |

| Forecast purchases | Regular GBP agency fees | Currency, average monthly spend |

| Natural offsets | EUR revenue that offsets EUR supplier costs | Currency, average monthly volume, timing |

Pull this data from your AP system, ERP, and purchasing team. Start by focusing on the top three to five currencies that make up 80% or more of your overseas spend. For most U.S. importers, this is typically EUR, CNY, GBP, JPY, and sometimes CAD or MXN, depending on supply chain geography.

Key questions your exposure map should answer:

- Which currencies drive the largest dollar value of overseas spend annually?

- How far forward are you exposed based on committed contracts and open POs?

- Do you have foreign currency revenue that naturally offsets any of your supplier exposure?

- What is the average lead time between placing an order and making the final payment?

- What is the maximum tolerable rate of movement before a deal becomes unprofitable?

Once you have this picture, you can make a rational decision about where hedging adds value versus where you can accept the natural movement.

Step 2: Understand the Three Types of FX Risk

Transaction Risk

This is the risk you take every time you agree on a price in a foreign currency before making the payment. If your supplier invoices you in euros and you pay 90 days later, the dollar cost of that invoice depends entirely on where the EUR/USD rate sits on payment day.

A 5% adverse move on a $500,000 annual supplier spend adds $25,000 to your costs with no change in what you ordered or received. At 10%, that becomes $50,000. These numbers are not theoretical. EUR/USD alone moved more than 8% in both directions during 2024.

Economic Risk

If the currencies of your primary supplier countries trend stronger against the dollar over a multi-year period, your input costs rise relative to competitors who source from countries with weaker currencies. This can gradually erode your pricing power and gross margin without any single dramatic event triggering a response.

Economic risk is harder to hedge with financial instruments. The best mitigation is supply chain diversification. Maintaining supplier relationships across multiple currency regions so no single currency trend has a dominant effect on your cost structure.

Translation Risk

For companies with overseas operations or subsidiaries, assets and liabilities denominated in foreign currencies change in reported USD value when exchange rates move.

This matters for consolidated financial statements, loan covenants measured in USD, and equity valuations. It is typically less operationally urgent than transaction risk, but matters at the board and investor reporting level.

Step 3: Choose Your FX Risk Management Strategy

Once your exposure is mapped, you choose how much of it to hedge and with what tools. The right approach depends on your risk appetite, the certainty of your cash flows, and the size of the exposure relative to your margins.

Operational Tactics (No Financial Products Required)

Before reaching for hedging instruments, look for ways to reduce your FX exposure through operational decisions. These cost nothing and can eliminate a meaningful share of your risk.

Negotiate invoice currency. For smaller or more transactional suppliers, negotiate to invoice in USD. Your supplier takes the FX risk. For key partners where you want favorable pricing, paying in their local currency often removes hidden FX markups they have built into USD quotes.

Shorten pricing windows. Avoid committing to fixed foreign-currency prices for 12 months without a hedge in place. Use 3 to 6 month pricing windows with review clauses tied to exchange rate bands.

Use natural hedges. If you have revenue in the same currency as your supplier costs. For example, EUR sales revenue that offsets EUR supplier invoices matches the timing of inflows and outflows to net your exposure before hedging the remainder.

Build FX clauses into long-term contracts. For large, multi-year supply agreements, negotiate a currency adjustment clause that triggers a price reset if the exchange rate moves beyond an agreed threshold in either direction.

Financial Hedging Instruments

For confirmed, material FX exposures that cannot be offset operationally, financial hedging locks in exchange rates and removes uncertainty from your cost of goods.

Forward contracts are the most commonly used instrument for supplier payment hedging. You agree with a bank or FX provider today to buy a specific amount of foreign currency on a specific future date at a fixed rate. The rate is agreed now, regardless of where the market moves between now and the payment date.

Forward contracts work best when your payment timing and amounts are reasonably certain, confirmed POs, contracted orders, or regular recurring invoices. The key risk is that if your payment does not materialize as expected (an order is cancelled, a supplier delays), you are still obligated under the forward contract.

Window forwards work like standard forwards, but allow you to take delivery of the currency at any point within a defined window rather than on a single fixed date. This is useful when the invoice timing from a supplier is variable. You lock in the rate today but retain flexibility on the exact payment date.

FX options give you the right, but not the obligation, to buy currency at a set rate. Unlike forwards, if the market moves in your favor, you can choose not to exercise the option and transact at the better spot rate.

The tradeoff is that options require an upfront premium payment. Options are particularly useful for uncertain exposures, bids, early-stage supplier negotiations, or purchases that are probable but not yet contracted.

Which instrument to use: Use forward contracts for confirmed, scheduled payables. Use window forwards when timing is uncertain, but amounts are known. Use options when volumes are uncertain or when the exposure relates to a bid or uncommitted purchase.

Step 4: The Best FX Risk Management Tools and Platforms

Executing an FX risk management strategy requires tools that can track exposures, execute hedges, and performance report. Here is a breakdown of the best options by company size and complexity.

Comparison Table

| Platform | Best For | Key Capabilities | Pricing |

|---|---|---|---|

| Kyriba | Large enterprise | Full TMS + FX exposure analytics + automated hedging | Custom ($150K+ annually) |

| GTreasury | Mid-market to enterprise | FX forecasting + hedge accounting + IFRS 9 compliance | Custom |

| Nomentia | Mid-market modular | FX derivatives + exposure tracking + ERP integration | Custom |

| Corpay | Mid-market payments | Multi-currency payments + forward contracts + FX platform | Custom |

| Xe for Business | SMB to mid-market | Forward contracts + rate alerts + multi-currency accounts | Low/no monthly fee |

| Ebury | SMEs needing trade finance | FX + forward contracts + letters of credit | Custom |

1. Kyriba

Best for: Large enterprises managing FX exposure across multiple entities and currencies

Kyriba is the leading enterprise TMS platform and includes a comprehensive FX risk management module that tracks currency exposure across subsidiaries in real time, recommends hedging strategies based on your policy, and executes FX forwards and options directly through the platform.

The AI-driven exposure aggregation automatically consolidates FX positions across entities and netting groups, which is critical for multinationals where the same currency exposure exists in multiple parts of the business. Kyriba also handles the full hedge accounting workflow for IFRS 9 and ASC 815 compliance, including documentation, effectiveness testing, and journal entry generation.

What Kyriba does well:

- Real-time FX exposure tracking and netting across global entities

- AI-powered hedging recommendations aligned to your treasury policy

- Direct integration with trading venues for hedge execution

- Full IFRS 9 and ASC 815 hedge accounting support

- Connects to 9,900 banks globally

Best for: Multinational enterprises with complex, high-volume FX exposures requiring enterprise-grade risk management integrated with their broader treasury operations. See our full review in the best treasury software guide.

2. GTreasury

Best for: Mid-market to enterprise companies with active hedging programs and compliance requirements

GTreasury includes a dedicated FX risk management module with strong hedge accounting capabilities. It supports exposure identification, hedge strategy modeling, forward and option tracking, and the documentation required for IFRS 9 and ASC 815 compliance.

The platform’s API-first connectivity pulls FX exposure data from ERP systems in near real time rather than relying on daily file uploads, which means your hedge book stays current with minimal manual intervention. The scenario analysis tools let treasury teams model the P&L impact of different hedging strategies before committing.

What GTreasury does well:

- Strong hedge accounting with IFRS 9 and ASC 815 support

- Real-time ERP integration for live exposure data

- Scenario modeling and what-if analysis

- Clean, modern interface that finance teams actually use

- Good mid-market pricing relative to enterprise TMS competitors

Best for: Mid-market and enterprise companies with active FX hedging programs that need both exposure management and hedge accounting in a single platform.

3. Nomentia

Best for: Mid-market companies wanting modular FX risk management alongside cash and payments

Nomentia’s FX derivatives module sits within its broader modular treasury platform. It supports exposure tracking, forward and option management, mark-to-market valuation, and compliance reporting. The modular approach means you can add FX risk management alongside cash management and payments without committing to a full enterprise TMS from day one.

Nomentia’s bank connectivity covers European and international banks well, and the platform integrates with SAP, Oracle, and Microsoft Dynamics for ERP data exchange.

Best for: Mid-market companies in Europe or internationally that want structured FX risk management as part of a broader modular treasury setup.

4. Corpay

Best for: Mid-market companies that want a payments platform with built-in FX risk capabilities

Corpay is a specialist cross-border payments provider that combines multi-currency payment processing with FX risk management tools. The platform supports forward contracts, rate alerts, multi-currency accounts, and bulk payment processing, all within a single interface that connects to your AP workflow.

For mid-market companies that do not need a full TMS but want more FX capability than their bank’s standard portal offers, Corpay sits in a practical middle ground. It handles both the execution of hedges and the payment of supplier invoices, reducing the number of systems your AP team needs to work across.

What Corpay does well:

- Combines FX hedging and international payments in one platform

- Forward contracts and rate protection available alongside payment processing

- Bulk payment uploads and AP workflow integration

- Accessible for mid-market teams without dedicated treasury staff

Best for: Mid-market companies paying overseas suppliers in multiple currencies that want a payments-first platform with FX hedging capability built in.

5. Xe for Business

Best for: Smaller companies and SMBs taking their first steps in managing FX risk

Xe for Business is the business-facing arm of Xe, one of the most recognized names in currency exchange. It offers forward contracts, limit orders, market orders, and multi-currency accounts through a straightforward online platform that does not require treasury expertise to navigate.

The platform is accessible for smaller finance teams that are moving beyond bank spot rates for the first time. You can set rate alerts, lock in forward rates for upcoming supplier payments, and hold multiple currency balances without the cost and complexity of an enterprise FX platform.

What Xe for Business does well:

- Simple, accessible interface for non-treasury teams

- Forward contracts for locking in rates on upcoming payables

- Rate alerts when target levels are reached

- Multi-currency accounts for holding foreign currency balances

- Low barrier to entry with transparent pricing

Best for: Small and mid-sized businesses that want to start managing FX risk on supplier payments without enterprise tools or dedicated treasury staff.

6. Ebury

Best for: SMEs that need FX hedging combined with trade finance solutions

Ebury combines FX services with trade finance, making it a strong fit for businesses that need currency risk management alongside financing solutions like letters of credit or invoice financing for international trade. It offers forward contracts, multi-currency accounts in over 29 currencies, and dedicated relationship managers for larger accounts.

The trade finance angle differentiates Ebury from pure FX platforms. For companies that finance their overseas supplier purchases through letters of credit or need import financing, having both services in one provider reduces friction.

Best for: SMEs engaged in international trade that need both FX hedging and trade finance capabilities from a single provider.

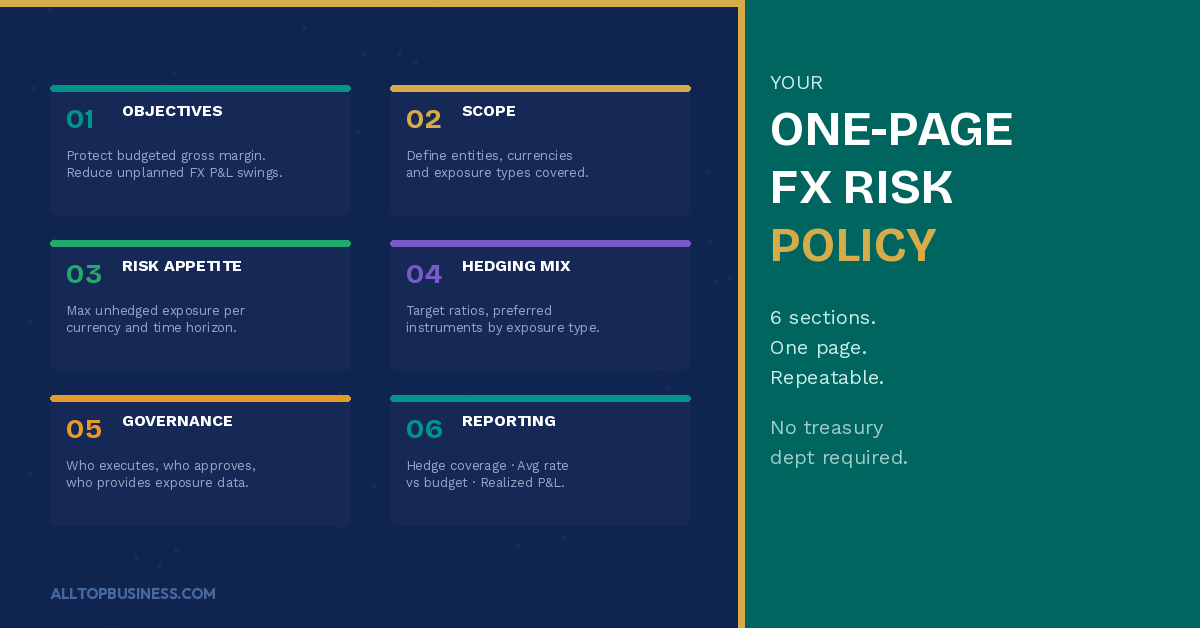

Step 5: Build a One-Page FX Risk Policy

A one-page FX policy turns ad-hoc hedging decisions into a consistent, auditable process. You do not need a 50-page governance document. You need a clear framework that tells your team what to hedge, how much to hedge, and who approves it.

Here is the structure that works for most mid-market companies:

1. Objectives: Define what you are trying to protect. For most supplier-facing companies, the objective is to protect budgeted gross margin on overseas purchases and reduce unplanned P&L swings from currency movements.

2. Scope: List which entities, currencies, and exposure types fall under the policy. Focus on currencies that represent more than 5% of annual overseas spend.

3. Risk appetite: Define how much unhedged exposure you are willing to hold per currency and per time horizon. For example: a maximum of $500,000 unhedged EUR payables at any time, and no unhedged exposure beyond 90 days without CFO approval.

4. Hedging approach: Specify your target hedge ratios and preferred instruments:

- 70% to 90% of booked payables in major currencies are hedged within 30 days of confirmation

- Forward contracts for confirmed orders and POs

- Window forwards where payment timing is uncertain

- Options for unconfirmed or bid-stage exposure

5. Governance Clarify who can execute hedges, who approves above-defined thresholds, and who provides exposure data. A clean structure for a mid-market company: AP team provides weekly exposure data, treasury or CFO executes hedges, board approval required for any hedge above $1 million notional.

6. Reporting Track three metrics at minimum: hedge coverage ratio by currency, average hedged rate versus budget rate, and realized FX gain or loss on closed positions. Review the policy annually or after any major shift in your supplier base or revenue mix.

The Most Common FX Risk Mistakes Mid-Market Companies Make

1. Hedging more than the underlying exposure.

Over-hedging creates speculative positions. Only hedge amounts and currencies tied to real underlying payables or purchase commitments.

2. Using the wrong instrument for uncertain volumes.

Forward contracts on purchases that never materialize leave you obligated to buy currency you do not need. Use options or window forwards for uncertain exposures.

3. Waiting too long to start hedging.

Most companies start thinking about hedging after a painful rate move has already happened. Building a routine hedging process when your margins are healthy is far easier than doing it reactively under pressure.

4. Not tracking realized FX performance.

If you never measure what you actually paid versus your budget rate, you cannot know whether your hedging program is working. Basic tracking takes 20 minutes a month and gives you the data to improve your approach over time.

5. Treating bank spot rates as the default.

Banks build FX margins into spot transactions that are rarely visible on the invoice. Specialist FX providers and platforms consistently offer tighter spreads on cross-border payments than commercial bank standard rates.

For companies making regular overseas supplier payments, the difference compounds into material savings over a year.

Frequently Asked Questions

What is FX risk management for supplier payments?

FX risk management for supplier payments is the process of identifying, measuring, and reducing the financial impact of exchange rate movements on your overseas purchasing costs.

It involves mapping your currency exposure, selecting hedging instruments like forward contracts or options to lock in rates on future payables, and tracking performance against your budget rates.

What is the simplest way to hedge supplier FX risk?

The simplest approach is a forward contract with your bank or a specialist FX provider. You agree today on the rate at which you will buy a set amount of foreign currency on a specific future date. This locks in your cost and removes rate uncertainty for that payable.

Most banks and platforms like Xe for Business, Corpay, and Ebury offer forward contracts with no complex setup required.

How much of my FX exposure should I hedge?

Most treasury policies target 70% to 90% coverage of confirmed payables in major currencies. You hedge confirmed orders and POs where the amount and timing are reasonably certain.

You leave unconfirmed or forecast exposure partially or fully unhedged, or use options for protection without full commitment. Hedging 100% of forecast purchases that may not materialize creates its own risk.

What is the difference between a forward contract and an FX option?

A forward contract is an obligation to buy a set amount of currency at a fixed rate on a fixed date or within a window. You must transact regardless of where the market moves.

An FX option gives you the right but not the obligation to buy at the agreed rate. If the market moves in your favor, you can let the option expire and transact at the better spot rate. Options cost a premium; forwards typically do not.

Do I need treasury software to manage FX risk?

Not at the beginning. Small and mid-market companies can manage FX risk effectively using a structured spreadsheet to track exposures, forward contracts through a specialist provider like Corpay or Xe for Business, and a simple monthly review process.

Treasury software like GTreasury or Kyriba makes sense once your hedging program grows to a complexity level where manual tracking becomes a risk in itself.

How do I know if my FX risk management program is working?

Track three things: your hedge coverage ratio (what percentage of confirmed exposure is hedged), your average achieved rate versus the budget rate for each currency, and your realized FX gain or loss on closed positions each quarter.

If your average achieved rate is consistently close to your budget rate and your FX P&L line is small and predictable, your program is working.

Final Thoughts

FX risk management does not require a trading desk, a complex treasury system, or a team of specialists. It requires a clear picture of your currency exposure, a consistent process for deciding what to hedge and with what tools, and a simple policy that makes the approach repeatable without relying on whoever happens to be managing finance that quarter.

Start with the exposure map. Identify your top three currency exposures by annual spend. Put forward contracts in place on your next two to three confirmed payables in those currencies. Measure the result. Build from there.

The companies that manage FX risk well are not necessarily the ones with the most sophisticated programs. They are the ones who treat foreign exchange as a cost input to be managed rather than a force of nature to be absorbed.

For more tools and guides covering treasury management and B2B finance operations, browse the AllTopBusiness blog. To track how well your FX and treasury operations are performing, read our guide on treasury management KPIs every CFO should watch. Have questions about your specific situation? Contact our team directly.

External Sources:

- Association for Financial Professionals — FX Risk Management Resources

- Gartner Peer Insights — Currency Management Software Reviews

I’m Adeyemi Adetilewa, a Content Marketing and SEO Specialist, Digital Strategist, Entrepreneur, and the Editor of AllTopBusiness.com. With over 13 years of experience helping businesses scale through content-driven growth, I’m happy to share all the top business tools I have discovered with you here.