The best cash forecasting approach for small treasury teams combines a direct-method 13-week rolling forecast, a weekly update routine, and a tool matched to your team size.

The top cash forecasting tools for smaller teams are Float, Agicap, Jirav, and Trovata. For mid-market and enterprise teams, Kyriba, HighRadius, and Nomentia offer more depth. This guide covers the process, the methods, the tools, and a practical weekly cadence to make it all work.

Over 60% of treasury professionals say cash forecasting is the most challenging task their team handles, according to the AFP 2025 Treasury Benchmarking Survey. And according to an EY-Parthenon analysis of 2,400 major global companies, only 28% of cash forecasts fell within 10% of free cash flow targets.

Those numbers are not surprising if you have ever built a forecast for a small finance team. You are working with messy AR data, payment timing that shifts every quarter, ERP exports that need manual cleaning, and leadership asking for a cash update on the same day you are trying to close the month.

The good news is that a reliable cash forecasting process does not require a large team, an enterprise TMS, or perfect data on day one. It requires a clear method, a consistent weekly rhythm, and a tool that matches your actual situation, not the one you might have in three years.

This guide gives you all three. It covers the core forecasting methods, the best tools for small and mid-market treasury teams, a practical week-by-week routine for standing up your process, and a weekly cadence checklist you can use immediately.

For context on where cash forecasting fits within the broader treasury function, read our guide on what treasury management is and how it works.

What is Cash Forecasting?

Cash forecasting is the process of projecting future cash inflows and outflows to understand your company’s liquidity position over a defined time horizon. A good forecast models expected customer collections alongside planned disbursements; payroll, vendor payments, debt service, taxes, and capital expenditures; to show projected cash balances across days, weeks, or months.

The output is not just a number. It is a decision-making tool. A reliable forecast tells you:

- Whether you have enough cash to meet obligations in the next 30, 60, and 90 days

- Where are the biggest risks to your cash position hiding

- Whether planned investments, hiring, or spending are financially sustainable

- When to draw on a credit facility before you actually need it

Cash forecasting is not the same as cash reporting. Reporting tells you what happened. Forecasting tells you what is coming and gives you time to act.

The Three Cash Forecasting Time Horizons

Not every forecast serves the same purpose. The right horizon depends on the decision you are trying to support.

Short-term (daily to 13 weeks).

The 13-week rolling forecast is the workhorse of treasury operations. It focuses on near-term liquidity, covering upcoming payroll runs, vendor payment cycles, tax obligations, and expected customer receipts. This is where cash crises get caught or missed. Most small and mid-market treasury teams should be running this forecast as their core operating document.

Medium-term (3 months to 12 months).

The medium-term forecast aligns projected cash with your operating plan. It answers whether planned hiring, marketing spend, or capital investment is financially sustainable over the coming quarters. This view feeds into budget conversations and board presentations.

Long-term (12 months and beyond).

Long-term forecasting supports capital planning and strategic decisions like debt capacity analysis, M&A evaluation, and long-term funding strategy. For smaller teams, this is typically a quarterly or annual exercise rather than a continuous process.

For most small treasury teams, the 13-week short-term forecast is where to start and where to spend most of your time. Get that right first before adding medium and long-term layers.

The Two Core Cash Forecasting Methods

There are two fundamental approaches to building a cash forecast. The right one depends on your data availability and forecasting purpose.

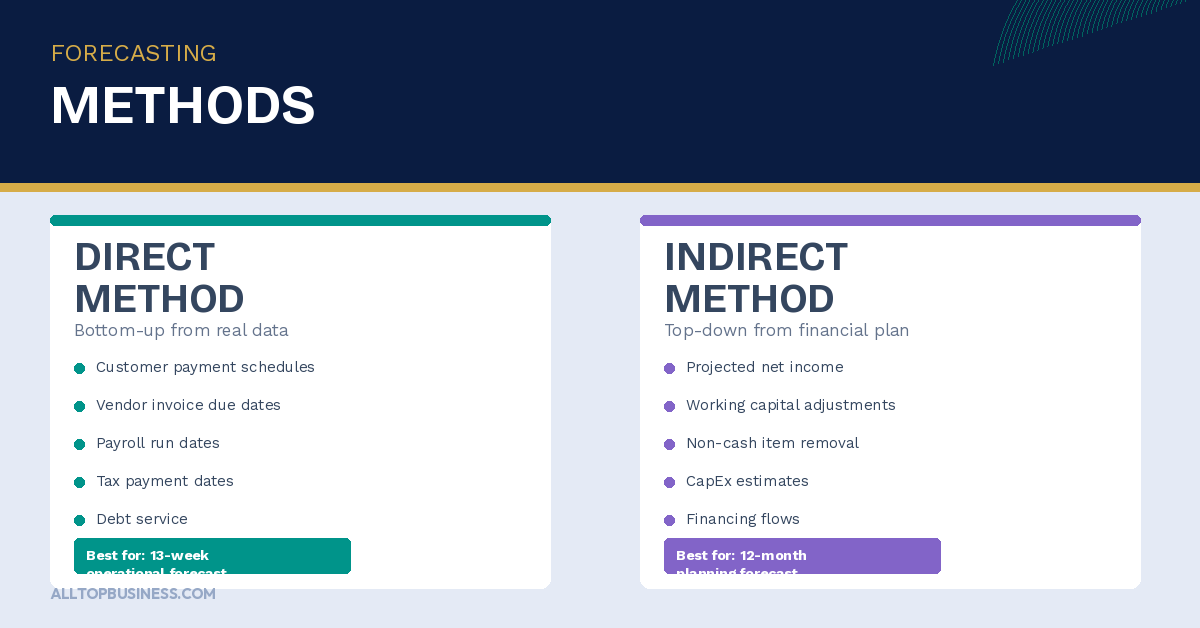

The Direct Method

The direct method builds a forecast from the bottom up by listing actual expected cash inflows and outflows line by line. You are working from real data: customer payment schedules, vendor invoice due dates, payroll run dates, known tax payments, and scheduled debt service.

This method is more accurate for short-term forecasts, particularly in the 13-week window, because it reflects what is actually in your AP and AR pipeline rather than high-level accounting assumptions. The tradeoff is that it is more data-intensive and requires good collaboration with the people who own AR, AP, and payroll data.

For small treasury teams, the direct method is the right approach for your weekly 13-week forecast.

The Indirect Method

The indirect method starts with projected net income from your financial plan and adjusts it for non-cash items and working capital changes to arrive at estimated cash flow. It is top-down and faster to build, which makes it useful for medium and long-term forecasts where line-by-line precision is neither possible nor necessary.

The indirect method is better for planning purposes than for operational cash management. If your CFO needs a cash outlook for the next 12 months for a board presentation, the indirect method gets you there efficiently. If your treasury team needs to know whether there is enough cash to run next Friday’s payroll, the direct method is the only one you should trust.

Most effective approach for small teams: Use the direct method for your 13-week operational forecast. Use the indirect method for medium and long-term planning that feeds into budget and board documents.

8 Best Cash Forecasting Tools for Treasury Teams

Choosing the right tool depends on your company size, ERP environment, and where your forecast currently breaks down. Here is a clear breakdown of the best options by use case.

Comparison Table

| Tool | Best For | Pricing | Key Integrations |

|---|---|---|---|

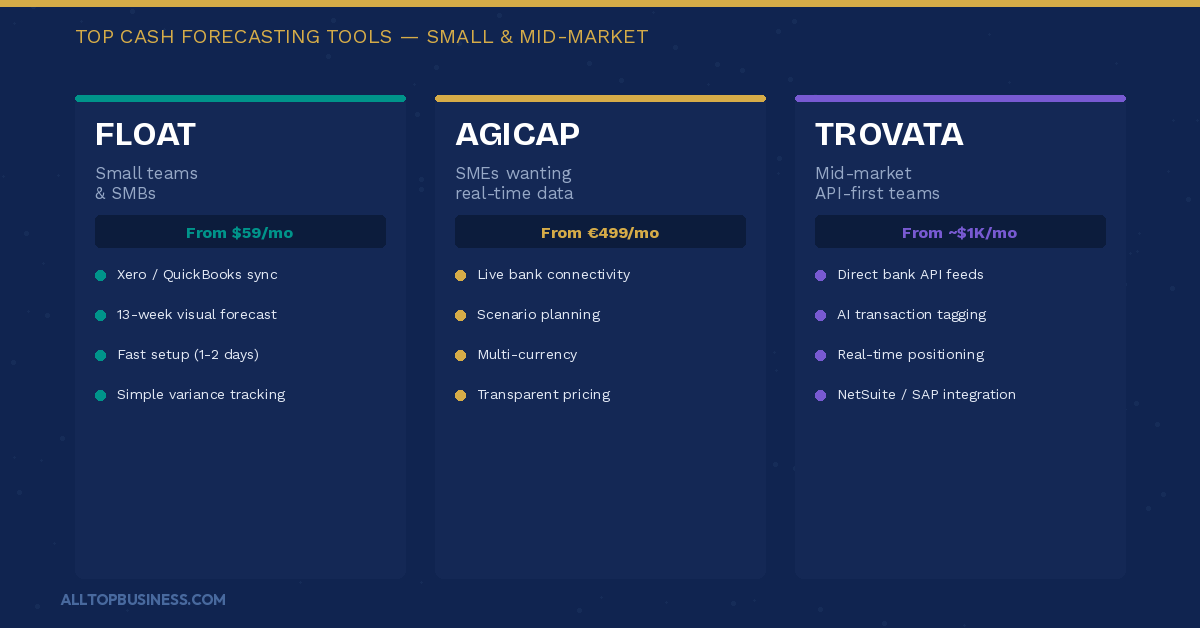

| Float | SMBs needing quick 13-week visibility | From $59/mo | Xero, QuickBooks, FreeAgent |

| Agicap | SMEs wanting real-time cash planning | From €499/mo | Xero, QuickBooks, Datev |

| Cash Flow Frog | Very small teams are new to forecasting | Free tier available | Xero, QuickBooks |

| Jirav | Mid-market with driver-based modeling | Custom | QuickBooks, Xero, NetSuite, HR systems |

| Trovata | Teams wanting real-time bank API data | From ~$1,000/mo | NetSuite, QuickBooks, SAP |

| HighRadius | Enterprise AR + treasury forecasting | Custom | SAP, Oracle, NetSuite |

| Kyriba | Global enterprise treasury | Custom | SAP, Oracle, NetSuite |

| Nomentia | Mid-market multi-entity treasury | Custom | SAP, Oracle, Microsoft Dynamics |

1. Float

Best for: Small and mid-sized teams that need fast 13-week cash visibility

Float is purpose-built for short-term cash flow forecasting. It connects directly to your accounting software (Xero, QuickBooks, or FreeAgent) and automatically builds a visual cash flow forecast from your accounting data without requiring manual input.

The setup is fast, and the interface is clean. A small finance team can typically be operational within a day or two. Float’s core strength is in giving teams a clear picture of their 13-week cash position without rebuilding everything in a spreadsheet.

Where Float falls short is when forecasting needs to go deeper than visual liquidity planning. It lacks rigorous forecast accuracy tracking, driver-based variance analysis, and enterprise-grade controls. For teams whose forecast needs to become a governance document reviewed by auditors or lenders, Float can feel lightweight.

Best for: Small businesses and lean finance teams that want to get off spreadsheets quickly and build 13-week cash visibility without a complex implementation.

2. Agicap

Best for: SMEs that want real-time cash visibility with scenario planning

Agicap connects to bank accounts and accounting systems to pull live transaction data, then lets finance teams build cash flow forecasts, track variances against plan, and run multiple scenarios. Its interface is notably more accessible than most treasury tools, and implementation typically takes days rather than weeks.

Agicap works well for companies with relatively straightforward cash structures, a small number of bank accounts, a single entity, and no complex intercompany or derivative requirements. For teams that have been managing cash in spreadsheets, Agicap is often the most practical next step.

Pricing starts from around 499 euros per month, making it one of the few cash forecasting tools with transparent, accessible pricing for smaller businesses.

Best for: SMEs across Europe and internationally that want real-time bank connectivity, visual forecasting, and scenario planning without enterprise complexity or cost.

3. Cash Flow Frog

Best for: Very small businesses taking their first step beyond spreadsheets

Cash Flow Frog is a straightforward cash flow forecasting and management tool designed specifically for small businesses. It integrates with Xero and QuickBooks and provides simple visual forecasts, alerts when cash is projected to dip below a threshold, and a clean dashboard for tracking actuals against forecasts.

It is not built for complex treasury operations, multi-entity structures, or sophisticated variance analysis. But for a business owner or finance lead who has never had a structured cash forecasting process, Cash Flow Frog provides an accessible and affordable entry point.

Best for: Very small businesses or sole operators who need basic cash visibility and alerts without a background in treasury or accounting software.

4. Jirav

Best for: Mid-market companies that want driver-based cash forecasting connected to their financial plan

Jirav is a cloud-based financial planning platform that takes a driver-based approach to cash forecasting. Rather than simply pulling accounting actuals, Jirav lets you connect revenue assumptions, headcount plans, and expense drivers to your cash projections — which means your forecast automatically updates when business assumptions change.

It integrates with QuickBooks, Xero, NetSuite, and popular HR systems, so your cash flow forecast reflects current payroll and expense data automatically. Jirav’s dashboards are clean and board-ready, making it a strong choice for teams that need to present cash forecasts to investors or boards regularly.

Best for: Mid-market companies with 50 to 500 employees that want structured, driver-based cash modeling connected to their broader financial plan.

5. Trovata

Best for: Mid-market teams that want real-time bank data through direct API connections

Trovata connects directly to banks through open banking APIs rather than relying on overnight file uploads, which gives treasury teams near-real-time visibility into cash balances across all accounts without the data lag of traditional bank feeds.

The forecasting model is bottom-up, driven by actual bank transaction history and pattern recognition. For teams with multiple banking relationships that spend hours each week pulling cash positions manually from different bank portals, Trovata eliminates most of that work quickly after implementation.

The key limitation is that Trovata forecasts from bank data, not AR data. It does not know about unprocessed invoices, disputed amounts, or the sales pipeline. Customer payment behavior patterns are learned over time, which means early forecasts are less accurate than forecasts built on six or twelve months of transaction history.

Best for: Mid-market treasury teams with multiple banking relationships that want fast, automated cash positioning and short-term forecasting without a complex TMS implementation.

6. HighRadius

Best for: Enterprise teams that want AI-powered forecasting integrated with AR automation

HighRadius uses category-specific AI models that treat AR, AP, and payroll as separate forecasting problems rather than rolling everything into a single blended view. This approach produces more accurate forecasts in complex enterprise environments where cash movement is driven by many different systems and approval workflows.

The platform also automates the data collection that slows most forecast cycles — bank statement download and classification, ERP integrations, and variance analysis comparing projected against actual cash. For teams that previously spent two or three days each week assembling cash reports manually, HighRadius can dramatically reduce that effort.

Best for: Enterprise and upper mid-market finance teams operating within SAP, Oracle, or Workday environments that need cash forecasting as part of a broader treasury management and AR automation platform. See our full breakdown in the best treasury software guide.

7. Kyriba

Best for: Global enterprises that need cash forecasting as part of a full treasury workstation

Kyriba is one of the leading enterprise TMS platforms and includes a powerful cash forecasting module as part of its broader treasury suite. It uses AI-driven modeling to build short, medium, and long-term forecasts that pull automatically from bank feeds, ERP data, and treasury positions.

For organizations running treasury across multiple countries, currencies, and banking relationships, Kyriba provides the depth and connectivity that standalone forecasting tools cannot match. It is not the right choice for small teams. The implementation timeline and cost structure are built for enterprise complexity.

Best for: Large enterprises managing global treasury operations that need cash forecasting integrated with risk management, payments, and bank connectivity in a single platform.

8. Nomentia

Best for: Mid-market and enterprise teams that want modular cash management and forecasting

Nomentia is a modular treasury platform built for mid-market companies that have outgrown spreadsheets and basic accounting tools but do not need full enterprise TMS complexity. Its cash forecasting module aggregates data from multiple banks and ERP systems into a single view and supports variance analysis, scenario planning, and multi-entity consolidation.

Nomentia has particularly strong coverage of European banking relationships and is well-suited for companies operating across multiple entities in different countries. The modular approach means you can start with cash management and forecasting and add payments, FX, or loan management as your needs grow.

Best for: Mid-market and enterprise companies in Europe or internationally that need structured multi-entity cash forecasting with strong bank connectivity and room to add treasury modules over time.

The Week-by-Week Cash Forecasting Routine

Once you have selected a tool, the process for standing up a reliable forecasting routine follows the same pattern regardless of team size. Here is a four-week build followed by a steady-state weekly cadence.

Week 1: Build Your Forecasting Baseline

Your goal in week 1 is a working first-pass 13-week forecast, not a perfect one.

Start by mapping your cash model. List opening cash balance, expected inflows like customer receipts, any funding tranches, interest income, and all outflows: payroll, rent, vendor invoices, tax payments, debt service, and any large one-off items you know about.

Use weekly time buckets rather than daily. You can always add granularity once the structure is working. For customer payment timing, use conservative assumptions based on your actual DSO history, not contracted payment terms. Most customers pay later than the terms.

Pull at least 13 weeks of historical bank and accounting data to shape your baseline assumptions. Actual payment patterns from your AR aging report will tell you far more about realistic collection timing than your standard net-30 payment terms.

Week 2: Tighten Your Short-Term View

Zoom in on the next four weeks. This is where cash risk usually surfaces first and where your forecast needs to be most accurate.

Run three checks every week during this phase:

AR reality check: Sit with the collections team or review AR aging directly. Which large invoices are due? Which customers are running late? Adjust your inflow assumptions accordingly.

AP and commitments review: Confirm which vendor invoices fall due in the next 30 days, plus payroll dates, tax deadlines, and any scheduled loan payments. Add any large uncommitted items you know are coming.

Bank balance reconciliation: Tie your forecast opening balance to your actual current bank balances. If these do not match, find out why before going further.

By the end of week 2, your 4-week forecast should be reliable enough that leadership can make spending decisions against it.

Week 3: Add Variance Analysis and Scenarios

With a working baseline and a reliable 4-week view, week 3 is about building control and learning.

Start your variance analysis routine. Compare last week’s forecast to what actually happened, line by line. Identify the top three misses and document why each one occurred. Late customer payment? Unexpected vendor invoice? Payroll timing shift? Every variance you root-cause makes your next forecast more accurate.

Build two simple scenarios on top of your base case: a downside scenario where your largest customer pays 15 days late, and an upside scenario where a pending deal closes on time. You do not need complex models. Even a basic sensitivity analysis on your top three inflow drivers tells you how much buffer you actually have.

Week 4: Systematize and Simplify

By week 4, you have a working model, a variance review habit, and a sense of where your forecast tends to miss. Now make the process light enough to sustain with a small team.

Look for four things to automate or simplify:

- Connect bank feeds directly to your forecasting tool rather than downloading and uploading manually

- Set up a standard weekly data request to sales and operations, so inputs arrive on a consistent schedule

- Create a one-page weekly cash summary template with the same structure every week

- Remove categories with less than 2% of total cash flow and group them into an “other” bucket

The goal is a weekly update cycle that takes 60 to 90 minutes, not half a day.

Weekly Cadence Checklist

Once the four-week build is complete, your steady-state routine should look like this:

Monday morning (30 minutes)

Update opening bank balances. Sync accounting data or check bank feed connections. Roll the forecast forward one week and archive last week’s actuals.

Midweek check (15 minutes)

Confirm any large receipts or payments expected that week. Flag anything that has shifted since Monday with a quick note in your forecast file.

Friday close (30 minutes)

Run variance analysis for the week. Note the top two or three misses and their causes. Refresh your downside scenario if anything material has changed. Send a five-line cash summary to your CFO: opening balance, projected low point over the next 13 weeks, top three risks, and any recommended actions.

Keep the summary tight. Opening cash, projected trough, biggest risks, and what you recommend doing about them. That is all your leadership team needs to make decisions.

The Most Common Cash Forecasting Mistakes Small Teams Make

1. Trusting contracted payment terms instead of actual payment history.

Net-30 terms mean nothing if your customers pay in 45 days on average. Always base your AR inflow assumptions on actual DSO history, not invoice terms.

2. Building the forecast once and not updating it.

A 13-week forecast that gets rebuilt quarterly is not a treasury tool. It is a budget exercise. The value comes from weekly updates that keep it current and accurate.

3. Not doing variance analysis.

If you never look at why your forecast was wrong, it will keep being wrong in the same ways. Twenty minutes of variance analysis each week is the fastest way to improve your forecast accuracy over time.

4. Over-engineering the model.

A 500-row spreadsheet with daily buckets and 40 line items sounds thorough. In practice, it is so complex to maintain that it stops getting updated. Start simple and add detail only where it genuinely changes a decision.

5. Forecasting in isolation.

Your cash forecast is only as good as the inputs from sales, procurement, and HR. Building a lightweight input process that gets you updated data from those teams each week is more valuable than any model sophistication.

Frequently Asked Questions

What is a 13-week cash forecast?

A 13-week cash forecast is a rolling short-term projection of your company’s expected cash inflows and outflows over the next 13 weeks.

It is the standard operating forecast for most treasury and finance teams because it covers a full quarter of visibility while remaining granular enough to manage near-term liquidity risk. It is updated weekly by rolling forward one week and adding actuals for the week just completed.

What is the direct method of cash forecasting?

The direct method builds a cash forecast from the bottom up by listing expected inflows and outflows line by line, like actual customer payment schedules, vendor invoice due dates, payroll runs, and tax payments.

It is the most accurate method for short-term forecasting because it reflects what is actually in your AR and AP pipeline.

How accurate should a 13-week cash forecast be?

Top-performing treasury teams target 85% to 95% accuracy at the 4-week horizon and 75% to 85% at the 13-week horizon. Below 70% accuracy at any horizon indicates a data quality or process problem that needs to be addressed.

Accuracy typically improves significantly once teams implement weekly variance analysis and start rooting out the recurring causes of forecast misses.

What is the best cash forecasting tool for a small business?

Float and Agicap are the strongest options for small businesses. Float is simpler and faster to set up for teams already using Xero or QuickBooks. Agicap offers more scenario planning capability and real-time bank connectivity.

Cash Flow Frog is a good starting point for very small teams new to structured forecasting. The right choice depends on your accounting system and how much depth you need.

How long does it take to build a reliable cash forecast?

With the right tool and clean accounting data, a small team can have a working 13-week forecast within one to two weeks.

Building a genuinely reliable forecast with high accuracy, weekly variance reviews, and leadership trust typically takes four to six weeks of consistent updates as you clean data and improve your assumptions.

Should small treasury teams use a TMS or a standalone forecasting tool?

For most small and mid-market teams, a standalone cash forecasting tool is the right starting point. A full TMS adds high cost and complexity that is not justified until you have multiple banking relationships, multi-entity structures, active FX risk, or payment volumes that require formal controls.

Start with a forecasting tool, build your process, and evaluate a TMS when you have outgrown it. Our guide on the best treasury software solutions covers when the step up to a full TMS makes sense.

Final Thoughts

Cash forecasting is one of the highest-leverage habits a small treasury team can build. A reliable 13-week forecast, updated every week, variance-reviewed every Friday, and shared in a tight summary with leadership, gives your organization genuine financial visibility that most businesses of the same size do not have.

The process does not need to be complex. It needs to be consistent. Pick the right tool for your current situation, build the four-week routine outlined in this guide, and commit to the weekly cadence. Your forecast will get better every week as you close the gap between what you expected and what actually happened.

For more on how to track the performance of your treasury function once your forecasting process is running, read our guide on treasury management KPIs every CFO should track. And for a broader view of the tools available to support your treasury operations, browse the AllTopBusiness blog or contact our team with any questions.

External Sources:

- Association for Financial Professionals — Cash Forecasting Benchmarks

- J.P. Morgan — Cash Forecasting Best Practices for Midsize Businesses

I’m Adeyemi Adetilewa, a Content Marketing and SEO Specialist, Digital Strategist, Entrepreneur, and the Editor of AllTopBusiness.com. With over 13 years of experience helping businesses scale through content-driven growth, I’m happy to share all the top business tools I have discovered with you here.